It’s no secret, I love credit union sales. My years serving credit union members through sales and leading sales teams taught me a lot about how to speak to, connect with, and engage credit union members in the sales process. And now I am equally excited and passionate about sharing it with all of my credit union clients.

As I visit credit unions across the nation to work with and train employees in sales, I see a consistent lack of cross selling incompetence. Inevitably this stems from employees not understanding how the products and services fit together, seeing the opportunity to cross-sell, and having the confidence to open the cross-sales discussion with the member. One way to help employees with this is to teach them how products and services your credit union offers fit together and complement each other.

Your credit union offers a lot of products and services to its members but they all filter down into one of two categories, core or ancillary products and services. When I teach this at first I get a lot of sideways glances and questions like:

“How can you categorize our 50 different credit union products into 2 categories?”

And…

“What in the world does ancillary mean?”

Core products are those that your member walks through the door asking for. They stand on their own and they are the heart of your credit union’s member solutions. Products like checking, savings and lending.

Ancillary simply means supporting or accompanying. So an ancillary product would be a product that supports a core product. Your member likely cannot have an ancillary product without at least one core product. Products such as payment protection, online access, direct deposit, and automatic payment are a few examples.

Core and ancillary products and services work together to create an account offering, and solidifies the member relationships. When we talk about creating primary financial relationships we often measure how many core products the member is taking advantage of but what truly solidifies a PFI relationship is how many ancillary products the member is using. Why?

How difficult it is for you to switch checking accounts when all you have is a debit card? Not difficult at all right? But add direct deposit, bill pay, automatic loan payments, online and mobile access, and overdraft protection to that checking account and the thought of switching becomes less appealing (tack on great member service and you have a relationship for life).

For so many credit union sales employees, this is where they struggle and as a result the credit union and its membership miss out on the opportunity available to them. To teach employees how to cross sell and feel confident doing it I use a visual process called product mapping.

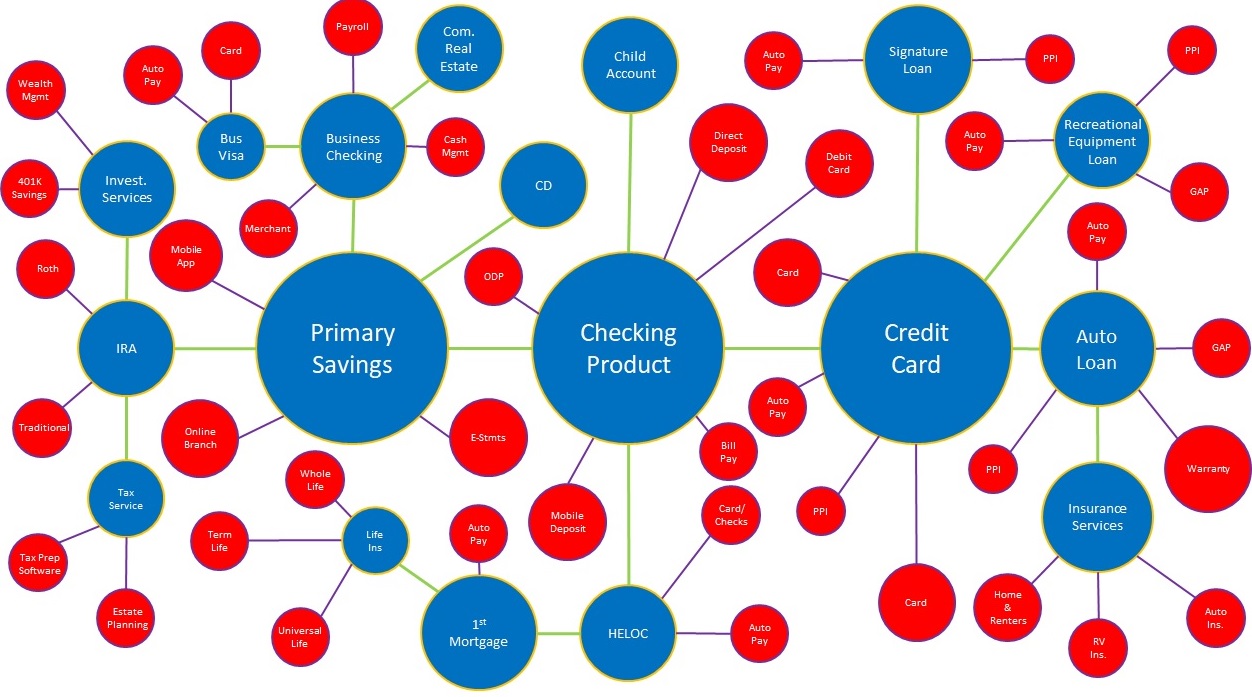

Product mapping is very simple and anyone who has been through product knowledge training can do it. Basically product mapping is identifying all of the ancillary products and services associated with a core in a way that looks similar to a map. With the product map in hand the sales employee can quickly see what products and services they should discuss and sell to a member opening a new core product. More importantly, the employee can use it to practice and polish their sales approach so when the member does come in they know what to say and are confident in the discussion.

Few things give me more satisfaction than when I see a credit union employee use the product map to identify cross selling opportunities on the teller line. When they pull up a members account they can use the product map to quickly identify the core products the member has and find ancillary products and services the member doesn’t have, but should. The map helps the employee remember what to look for and not get focused on just one or two products like auto pay or direct deposit. With product map training the tellers are equipped to sell a wide range of products and services to help their member with all of their financial needs.

The product map is so simple, but yet so effective. It is visual and something everyone can understand. What makes it so effective though is how easy it is for your branch, service center and outbound call center leaders to coach to. Even in shadow coaching situations when the member is present. Training the employee to use the product map, then reinforcing it with shadow coaching in their position quickly helps the employee to develop the skills and behaviors that make them competent cross sellers.

You can learn a little bit more about product mapping in this introduction video created for my online sales training course SalesCU.

What do you think? Would product mapping work for your credit union’s sales employees? Let me know your thoughts in the comments below.